Charter Report

Market Intelligence

2023 Asia-Pacific Charter Market Overview

This article is extracted from the most recent edition of Charter Report.To read the full…

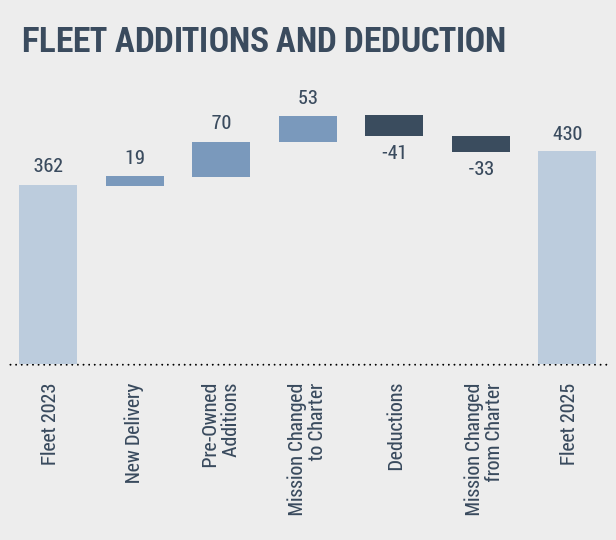

At the end of June 2025, there were 430 charter aircraft in the Asia-Pacific region, increasing from 362 at the end of June 2023.

Some 19 new-build aircraft were delivered to the Asia-Pacific region as charter aircraft, while 70 pre-owned aircraft joined the fleet. Additionally, there were 25 aircraft sold to other regions, as well as 16 aircraft stored or retired. Overall, the market demand in business jet charter rose between June 2023 and June 2025, especially in South Asia.

In June 2025, the number of private jets available for charter in the Asia-Pacific region increased by 18.8% compared with June 2023. Notably, all size categories experienced growth except for Corporate Airliners. The most significant increases were observed in Medium Jets and Very Light Jets, which expanded by 45.6% and 59.4% respectively, reflecting the emerging demand for both medium-haul and short-haul flight routes.

Long Range Jets remained the preferred category for AsiaPacific operators. Among them, the Gulfstream G650ER and G550 stood out as the top chartered models, with 20 and 18 aircraft in operation, respectively. Bombardier’s Global Express series followed closely behind as another highly sought-after option. This category saw growth, with charter fleet numbers increasing by ten compared to 2023. New Loong Airlines, founded in June 2024 by Nanshan Holdings, introduced three Gulfstreams into its management and charter fleet, including the first G500 and G700 delivered to mainland China.

Large Jet and Light Jet ranked as the second and third most popular categories for private jet charters, respectively. This demand reflected the charter needs between long-haul and costeffective travel. The Large Jet fleet in the Asia-Pacific region grew from 77 to 91 aircraft over the past two years, with the most significant expansion occurring in its largest market, India, where the Large Jet fleet expanded from 22 to 36 aircraft. The number of Light Jets in charter operation experienced a minor increase from 85 to 86 aircraft. This size category remained particularly popular in the Australian charter market, where Light Jets were also frequently deployed for medical charter missions. Notably, Pilatus’ PC-24 and Bombardier’s Learjet were among the most frequently employed Light Jets for regional patient transfers and medical staff transport. Embraer’s Legacy 600/650 series and Textron’s Citation series stood out as the most widely offered models among Large Jet and Light Jet categories.

Medium Jets represented 19.3% of the Asia-Pacific private jet charter market. These aircraft were capable of direct flights between major Asia-Pacific cities, including routes such as Mumbai–New Delhi and Sydney–Melbourne, making them ideal for business and short-haul travel. As of June 2025, a total of 83 Medium Jets were available for charter across the Asia-Pacific region. Within this size category, the Textron Citation 560XL, G100/G150, and Hawker 800/XP were the most popular models, with 13, 12 and 12 aircraft in operation, respectively.

Very Light Jets and Corporate Airliners occupied relatively small segments of the Asia-Pacific private jet charter market, accounting for 11.9% and 4.0% of total capacity, respectively. The Citation Mustang led the Very Light Jet segment with 20 aircraft, predominantly operated by charter providers from Australia and New Zealand, reflecting strong regional demand for short-haul, flexible point-to-point travel.

Corporate Airliners continued to serve as the preferred choice for government operations and large corporate groups, where seating capacity and comprehensive onboard facilities are critical. The Bombardier CRJ 100/200 series was the most widely utilized, with f ive managed by Chinese charter operators. As of June 30, 2025, there were 17 Corporate Airliners operating in Asia-Pacific for charter, representing a decrease of two aircraft compared with 2023.

Textron remained the largest OEM in the Asia-Pacific charter fleet, holding a market share of 30.9% as of mid-2025. Its Citation series continued to be the most popular charter model, particularly in India and Australia, where demand for Light and Medium size business jets has been consistently strong.

Bombardier experienced a modest increase in its Asia-Pacificbased charter fleet between mid-2023 and mid-2025, adding two aircraft, bringing its total fleet in the region to 103. During the period, two brand-new Bombardier Global jets entered the charter fleets in India and Malaysia, reflecting steady demand for longhaul business travel. Meanwhile, India and Indonesia emerged as the largest markets for Embraer’s Large Jets. Since June 2023, these two countries have seen 34 pre-owned Embraer aircraft added to their charter fleets. The average age of Embraer Large Jets in India and Indonesia exceeded 15 years old, slightly higher than the Asia-Pacific regional average.

Gulfstream’s charter fleet expanded from 57 aircraft at the end of June 2023 to 82 by mid-2025, representing a 43.9% growth rate. Some aircraft owners transition their jets from managed arrangements into charter operations, allowing operators to better align their fleets with the region’s growing demand for long-range travel, while also enhancing overall aircraft utilization.

Pilatus’ “super versatile jet” — the PC-24 — saw its charter fleet in the Asia-Pacific region grow from seven aircraft at the end of June 2023 to 15 by mid-2025. One of India’s largest charter operators, Karnavati Aviation under the Adani Group, acquired four brand new PC-24s during the past two years, serving short-range charter routes between India’s major cities.

At the country and regional level, charter fleet compositions across Asia-Pacific showed regional preferences. India, Australia, and mainland China — the region’s three largest charter markets — each favored different aircraft categories. In India, Large and Medium Jets together made up 57.9% of the charter fleet, offering both the connection between major Indian cities and the cabin comfort sought by ultra-high-net-worth and corporate clients. Australia, in contrast, showed a preference for Light and Very Light Jets, reflecting its extensive network of small airports and high demand for short-haul flights. Mainland China demonstrated stronger demand for Long Range Jets, supporting cross-border travel. Similarly, Japan relied predominantly on Long Range Jet charter services for intercontinental flights, which accounted for 32.4% of its charter fleet, while its locally preferred Light Jets and Very Light Jets made up 55.9% of the local charter market to support domestic flight demands.

Compared with privately owned business jets, charter aircraft in the Asia-Pacific region tend to be older, though most would undergo regular cabin refurbishments to ensure consistent customer experience. As of the end of June 2025, the average age of the charter fleet in the region stood at 15.9 years. New Zealand and Australia recorded the oldest fleets, with average ages of 22 years and 19 years, respectively. In India — the country with the largest charter fleet — more than half of the aircraft were more than 15 years old, while 16.0% were less than five years old. Among all size categories, Long Range Jets had the youngest charter fleet, averaging nine years, with 31.1% of the fleet under five years old.

Market Intelligence

Market Intelligence

Market Intelligence

2025 Q1

Business Aviation Business Aviation News – Q1 2025 Business Aviation BAAFEx Brings Shows Back To Asia See all articles

YE 2024

Business Aviation Executive Summary – Civil Helicopter Fleet Report YE 2024 Business Aviation The Asia-Pacific Offshore Helicopter Fleet See all articles

YE 2023

Business Aviation First To Fly: Dassault Falcon 6X Business Aviation CorporateCare Enhanced: Keeping Business Jets Flying See all articles

YE 2023

Civil Helicopters Other Civil Helicopter Fleet Report YE 2023 – Executive Summary Civil Helicopters eVTOL OEMS in Asia-Pacific See all articles

2023 Q2

Business Aviation Signature Revamps Anchorage FBO Business Aviation Dassault’s Asia Pacific Strategy See all articles

YE 2022

Civil Helicopters Helicopter Spotlight: Airbus H175 See all articles

2022 Q4

Business Aviation New, Big Falcons Suit Asia-Pacific Business Aviation Supporting Modern Time Machines See all articles

YE 2022 - Europe

Business Aviation Luxaviation CEO Sees Deficiencies in Seemingly Buoyant Market Business Aviation Supporting Modern Time Machines See all articles

YE 2022 - MENA

Business Aviation DC Aviation Al-Futtaim Celebrates Ten Years in the Middle East See all articles

YE 2021

Business Aviation Market Trends – Business Jet Fleet Report YE 2021 Business Aviation 10 Year Forecast See all articles

YE 2021

Civil Helicopters Leasing Market – Civil Helicopter Fleet Report YE 2021 Civil Helicopters EMS Market – Civil Helicopter Fleet Report YE 2021 See all articles

2021 Q3

Other Pre-owned Market Spotlight: Citation Sovereign/Sovereign+ – Asian Sky Quarterly 2021 Q3 See all articles

YE 2019

Civil Helicopters EVTOL News in Asia – Civil Helicopters YE 2019 Civil Helicopters Engine OEM Overview – Civil Helicopters YE 2019 See all articles© Copyright Asian Sky Group -2025 | All Rights Reserved